Everything You Need to Know About Refinancing A Vacation Home

Homeowners looking to diversify their financial portfolio usually start with a vacation property to establish a solid foundation. Determining whether or not they can refinance the mortgage on that second property can be potentially volatile. Homeowners with more than one property want to find ways to streamline and maximize their mortgage payments on both properties. Determining whether or not your second home can qualify for a mortgage depends on multiple factors that can tip the scale in one direction or the other.

How Do You Use Your Second Home?

People use their second homes for various purposes. From pure vacation homes to Lake Tahoe rentals and a financial portfolio base, second homes wear many hats for homeowners. The nature of the second home will directly impact your ability to get a reasonable rate and refinance your second mortgage. Whether you use it exclusively as a vacation home or as predominantly a rental property will affect the types of rates you can get from a lender. If your vacation home falls under the qualifications for a rental property, you will not be able to refinance. You’ll have to provide proof that your second home does not fall under this category.

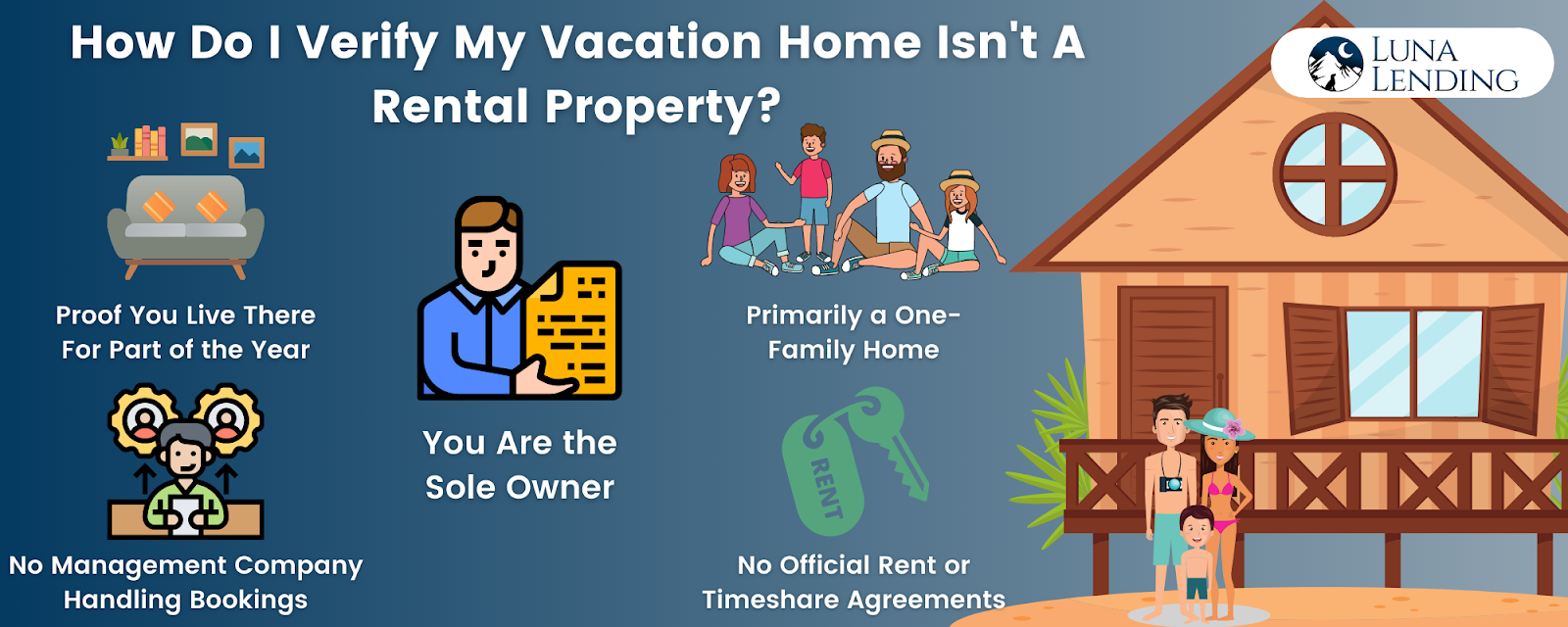

How Do I Verify My Second Home Isn’t a Rental Property?

To verify your second home does not qualify as a rental, you need to prove a few critical points. The following infographic outlines some of these factors:

Once you verify that your vacation home isn’t a rental, you can take steps to refinance your mortgage.

What Kind of Refinance Rates Do I Qualify For?

When you start exploring the finer points of “how do I go about refinancing my home?” you ultimately want to know what kind of rates you can get. Most lenders view vacation homes, and second homes in general, as a more volatile investment than primary homes, so they generally give you a higher rate. They take a macro view of the property’s mortgage; they see a secondary property as a secondary priority for the homeowner. If they fall behind on payments for one or either of their properties, they’ll be more likely to catch up and pay off their primary residence. While you can expect to get a higher rate for the secondary mortgage, there are still ways that you can bring that rate down a bit. If it’s the second time you have refinanced a secondary home, you’ll generally be viewed as reliable and may get a more favorable rate.

When you start refinancing your second home, you want a lender with experience dealing with secondary and vacation properties. With Luna Lending, you can rest assured that your secondary property is in good hands. Contact us to get your free rate quote and get the refinancing process started today!

AHL is an Equal Housing Opportunity Broker. NMLS: 17296528 DRE 02058505